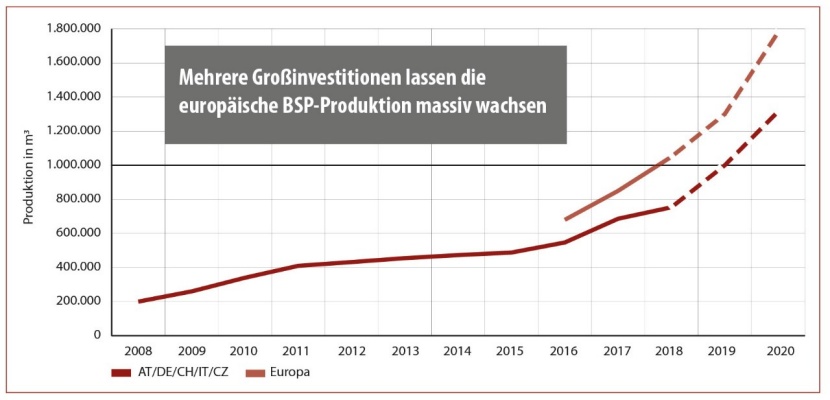

With annual growth rates beyond the 10% mark, the Central European CLT sector continues to increase considerably. In 2017, the produced volume in the "DACH" region (Germany, Austria and Switzerland), in Czech Republic and in Italy gained 15% totalling 690,000 m³; this year, the output will increase by another 13% to 770,00 m³. Growth is mainly due to production increases of almost all big producers (see table below). The two newcomers, Johann Pabst Holzindustrie, Zeltweg, and Best Wood Schneider, Eberhardzell/DE - both started producing CLT with 1.25 m width this year - are not considered here yet.

The growth curve of upcoming years is expected to be even steeper: In 2019, the Derix group in Westerkappeln/DE and Schillinger Holz in Küssnacht/CH are launching new large-scale production lines. Furthermore, the Pfeifer Group will enter the sector with a 100,000 m³ factory in Schlitz/DE and Stora Enso is launching a third factory in Scandinavia.

For 2020, the Johann Offner enterprise group announced the opening of a second KLH site in Wiesenau near Bad St. Leonhard. The final expansion will output 150,000 m³/yr of CLT. This would mean a total of 270,000 m³/yr for KLH - just like Binderholz and Stora Enso. Binderholz will reach this figure by means of a second expansion stage in Burgbernheim, and Stora Enso thanks to a third site in Gruvön/SE. Adding up the prospective capacities of the "big three", the sum of 800,000 m³ exceeds Central Europe's current total output. Next to these confirmed projects, there are several other Austrian and German timber industries that have concrete plans to enter the CLT market or expand existing capacities. However, nobody wanted to openly comment on these projects yet by the editorial deadline. Concerning the time after this announced surge in investments, machine suppliers have divided expectations. While part of them anticipate a "breather", other machine manufacturers reckon "further growth boosts" up to a "market doubling within a few years".

800,000 m³/yr: From 2021 onwards, three enterprises will be producing more CLT than today's sector in total.

Development of CLT production in Europe since 2008: Several major investments are boosting Europe's CLT production

© Timber-Online

Potential throughout Europe

Strong increases have also been observed for the Northern European market. After relatively small plants (up to 40,000 m³/yr) in Finland (CLT Finland), Latvia (Skonto Cross Timber Systems) and Sweden (Martinsons, Södra), now a large-scale project will be installed at Splitkon, Norway. Next up is Swedish timber industry Setra's start into the sector with a production capacity of 55,000 m³/yr, announced for 2020.

Södra is currently only running one test plant with 7000 m³ per year and shift, but is expected to extend it by a large-scale plant. Last but not least, the previously mentioned Stora Enso site in Gruvön/SE with a capacity of 100,000 m³/yr will be launched next year. According to industry experts, this is only the beginning since "the large timber industries have recognized the potential and CLT starts catching on on the market".

Less successful was the 120,000 m³/yr large-scale project by British insurance group Legal & General. The purchased facilities were never brought into operation - now they are looking for a buyer, as is known in the industry. In terms of delivery times, machine suppliers currently are not facing major problems.

Experts also see great potential in Eastern Europe, Russia and France where a few weeks ago, Piveteaubois launched a large CLT line.

A need to catch up in America

"Potential, yes - infrastructure and know-how, no." This is the gist of how some Central European experts see the North American market by and large. "If Europe is the Champions League, the United States constitute the second division", as one machine supplier put it. Despite several announced production lines and mega-projects, the breakthrough is still far from being achieved.

Apart from lacking capacities as well as experience in terms of production, the United States also needs planners and skilled staff. "Often, objects are built by steel constructors who lack know-how and experience in wood construction. This holds many sources of error", a European producer puts a finger on the problem. But despite - or exactly because of this, the US market receives intensive attention from European producers and machine suppliers.

University professor Dr. Gerhard Schickhofer at the Graz University of Technology sees the future of CLT in prefabrication and modulization: "After developing the product, now we have to focus on the construction practice. In close collaboration with building technicians and architects, we must look at the entirety of building, move away from known systems and focus on wood-appropriate solutions. A lot of steps that are now taken care of at the construction site could also be moved to the production hall." Tangibly implemented solutions in this field would considerably help boosting the global spread of CLT.

| Company | Location | Production 2017 (m³) | Production 2018 (plan; m³) | 1 shift capacity (m³) | Special features | Joint gluing | SF adhesive | Types of wood in SF | Format up to [m] |

|---|---|---|---|---|---|---|---|---|---|

| Agrop Nova | Ptení/CZ | 7,000 | 7,000 | n/s | Top layers without finger-joints; acoustic/rib/box elements |

yes | PUR, MUF | Spruce, fir, Sib. larch | 2.95 x 12 |

| Best Wood Schneider | Eberhardzell/DE | – | – | – | Production start 2018 | up to 1.25 width | |||

| Binderholz Bausysteme | Unternberg/AT, Burgbernheim/DE | 170,000 | 195,000 | 80,000 | System format BBS 125, large format BBS XL | for vis. quality | PUR | Spruce, larch, Swiss pine, silver fir, antique | 1.25 x 24; 3.5 x 22 |

| Eugen Decker | Morbach/DE | 25,000 | 25,000 | 25,000 | Special structures and formats | no | PUR | Spruce, Douglas fir, pine | 3.3 x 16 |

| W. u. J. Derix | Niederkrüchten/DE | 12,500 | 12,500 | 15,000 | virtually jointless gluing, CNC joining | 50% glued *** | MUF | Spruce, fir, larch, pine, Douglas fir | 3.5 x 18 |

| Hasslacher Norica Timber | Stall im Mölltal/AT | 38,000 | 55,000 | n/s | X-fix, SF finishing, excellent SF finish, order size = charging size, all SFs sanded |

upon request | MUF | Spruce, larch, pine, fir, Swiss pine, birch, oak | 3.2 x 20 |

| Kurt Huber | Achern/DE | 5,000 | 5,000 | 7,000 | individually tailored |

no | PUR | Spruce, fir | 3.8 x 19 |

| KLH Massivholz | Teufenbach-Katsch/AT | 110,000 | 120,000 | n/s | Project support, JAS, PRG 320, FSC, ISO 50001 | upon request | PUR | all softwoods, predom. spruce | 2.95 x 16.5 |

| Lignotrend | Weilheim/DE | 24,000 | 26,000 | n/s | CLT rib elements configurable (f. vis. qual., fire resistance, noise control) | n/s | PUR | Spruce, vis. SF silver fir etc. | up to 18 length |

| Mayr-Melnhof Holz | Gaishorn/AT | 70,000 | 75,000 | 25,000 | Pressing either on HF press or cold molding press | no | PUR, MUF | Spruce, larch | 3.5 x 16, 3.0 x 16,5 |

| Merkle Holz | Nersingen/DE | 1,000 | 1,000 | n/s | Joining and pre-assembly possible | no | MUF | Spruce, Douglas fir, larch | 0.72 x 18 |

| Johann Pabst Holzindustrie | Zeltweg/AT | – | – | – | Production start 2018; plan 2019: 10,000 m³ | MUF | Spruce |

1.25 x 17 | |

| Rubner Holzbau | Brixen/IT | 3,800 | 7,000 | 10,000 | - |

no | PU | Spruce, fir, pine | 4 x 17 |

| Schilliger Holz | Küssnacht/CH | 13,000 | 13,000 | 9,000 | order-related formats, top layers juncture glued | yes | PUR | all softwoods | 3.4 x 13.7 |

| Pius Schuler | Rothenthurm/CH | n/s | n/s | n/s | CLT pioneer |

n/s | n/s | Spruce, fir, pine, larch, Douglas fir | 3 x 9 |

| Stora Enso | Bad St. Leonhard | 72,000 | 80,000 | 90,000 | vis., industry vis., non-vis.; sanded, airtight from 3 layers, rib element production | yes | PUR | Spruce, pine, fir | 2.95 x 16; 3.95 x 16 (upon request) |

| Stora Enso | Ybbs/AT | 78,000 | 90,000 | ||||||

| Holzbau Unterrainer | Ainet/AT | 7,000 | 10,000 | 5,000 | curved CLT ("radius wood") from a radiuw of 1.2 m | no | PUR | Spruce, larch, Swiss pine | 2.95 x 13.5 |

| Weinberger Holz | Reichenfels/AT | 6,500 | 6,500 | n/s | settling-free log house plank crosslam. (plywood beams) | yes | PUR | Spruce, larch, pine, Swiss pine | 1.2 x 13.5 |

| XLam Dolomiti | Castel Ivano/IT | 13,500 | 15,500 | 9,000 | - |

no | PUR | Spruce | 3.5 x 13.5 |

| Züblin Timber | Aichach/DE | 30,000 | 30,000 | n/s | Format flexibility, special structures, superelevated and curved elements | no/on request for top layer |

PUR | Spruce, Nordic Spruce, Fineline, precious timber | 4.8 x 19.8 |

| Sum** | 686,300 | 773,500 |

| Company and location | 2017 | 2018 (plan) | Special features | Joining | Types of wood | Format up to [m] |

|---|---|---|---|---|---|---|

| Rombach Nur Holz, Oberharmersbach/DE | n/s | n/s | – | Beech bolts |

n/s |

3.2 x 12 |

| Thoma Holz 100, Lahr/DE, Stadl/AT | n/s | n/s | Moon timber, Wood100 system | Beech dowels | Spruce, fir, pine, larch | 3 x 8 |

| GT Systemfertigung, Lavamünd/AT; Sägewerk Meissnitzer, Niedernsill/AT; Abbundzentrum Dahlen, Dahlen/DE; Das Naturholzhaus, Dinkelsbühl/DE; Holz in Form, Rothenkirchen/DE; Holzbau-Binz, Ellwangen-Pfahlheim/DE; Herrmann Massivholzhaus, Geisa an der Rhön/DE; MHM Abbundzentrum, Oelde/DE; Inholz, Mannheim/DE; Holzbau Bendler, Nordrach/DE; Holzbau Koch, Ainring/DE; Veit Fröhler Bau, Hutthurm/DE; Zimmerei Karrer, Woringen/DE; Zimmerei Mayr & Sonntag, Legau/DE; R3 Massivholzhaus, Asch/DE; Zimmerei Thumann, Berg Hausheim/DE; Gauye & Dayer Charpente, Sion/CH; MHM Schweiz/Haudenschild, Niederbipp/CH | 44,000 | 45,000 | gesammelte Produktionsmenge der Hersteller des Systems „Massiv-Holz-Mauer“ im DACH-Raum | Aluminium groove pins | n/s |

4 x 6 |