In order to understand 2021, one has to analyze 2020. In that year, the lockdowns, which were imposed to limit the spread of COVID-19, led to a decrease in global softwood lumber production. At the same time, people had the time and money to improve and modernize their houses for which they also needed a lot of lumber. As a result, demand grew.

2020 deficit felt in 2021

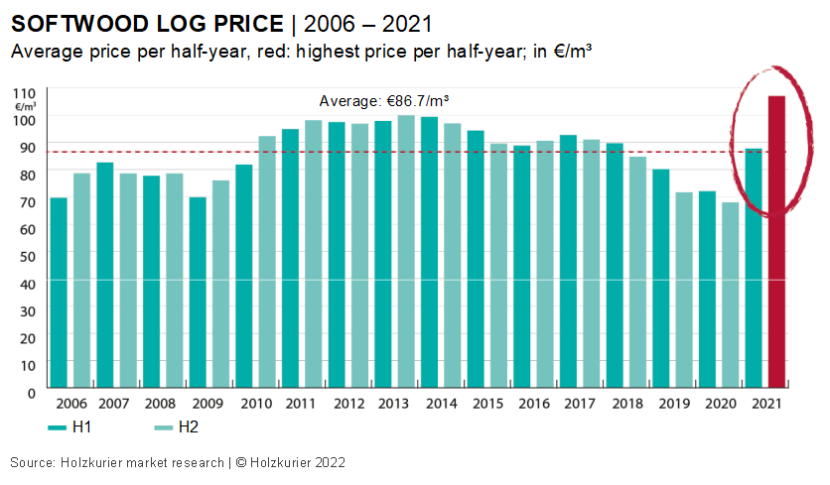

In 2020, demand for softwood lumber exceeded supply by around 14 million m³. The industry really felt the effect of this deficit in the first half of 2021. A harsh winter in Scandinavia and a lot of snow in Austria led to reduced cutting in sawmills and, as a result, to empty warehouses of retailers, timber construction companies and producers.

Build-up in demand

The panic situation that followed led to a bullwhip effect: The timber construction company orders 1 m³ of glued timber. The retailer notices that delivery times are long and orders 2 m³ from the wholesaler just to be on the safe side. The wholesaler knows that prices are rising and that producers are only delivering small quantities and orders 4 m³ from the industry – and nobody notices that there are so many caution, phantom and panic orders in the sales process.

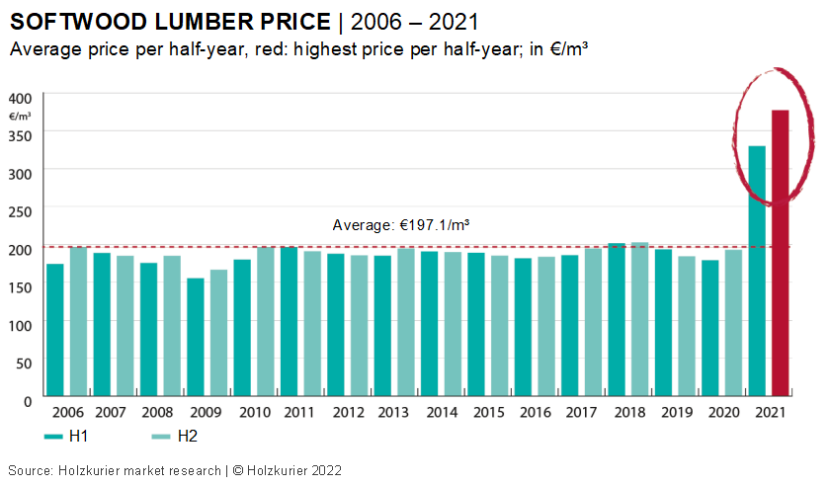

At the same time, producers send out price lists with projections about how high prices will likely be in two or three months. This further spurs purchases according to the motto: “Quantity before price.” The US softwood lumber price reaching nearly €900/m³ in May 2021 did the rest.

Two overheated regions

It has to be said, however, that there were only two completely overheated regions at a global level:

- the US

- Germany, Austria, Switzerland and Italy.

Japan only accepted the price increases up to a certain point. China’s reaction was completely different. Instead of importing lumber, Chinese buyers turned to log wood as an alternative. As for the latter, availability was better throughout the entire year. Also, prices were lower.

Marked decrease but at a high level

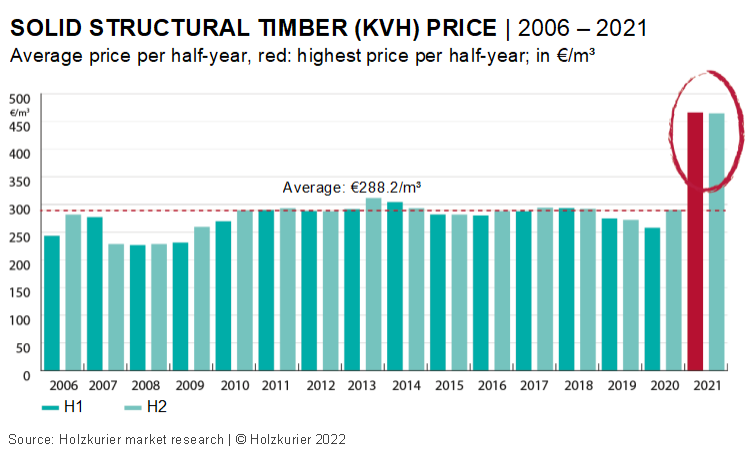

The upward trend of lumber prices ended in June/July. Since then, prices have fallen considerably, that is by 40 to 50% from July to December. Now, at the turn of the year 2021/2022, however, prices are still much higher than they were in the same period of previous year.

Austria was under a blanket of snow at the end of 2021. Sawmills shut down for three weeks which is also unique.

Demand to remain strong in 2022 as well

There is consensus among market experts that demand for softwood lumber will remain at least as high in 2022 as it was in 2021 and that it will likely see strong growth again. Now, the key questions are when it will take off again and whether there will be enough wood by then.

Logistics possibly more challenging in 2022

Additionally, there is no guarantee that customers will even receive goods just in time. Also, there is hardly any doubt about one other thing: Logistics will remain a major challenge in 2022 and the situation could get worse since there is a shortage of truck drivers around the world and shipping space is scarce.

Demand for softwood lumber will increase this year due to the high level of construction activity around the world. The Holzkurier predicts a further growth in demand in 2023.

European lumber producing countries were already close to the limit in 2021. The European Organization of the Sawmill Industry expected a 7% increase in production in 2021. As this was already a record level, production is projected to grow by only 0.6% this year. Demand, on the other hand, will increase by at least 1.5%.

According to Don Kayne, CEO of Canfor, the biggest sawmill group in the world, there won’t be a balance between supply and demand on the global softwood lumber market before 2025. Then, Europe will be the global leader with a production of 165 million m³ and a demand of 144 million m³.

Still a lot of damaged wood

Despite all the optimistic forecasts regarding demand, one must not forget that Central Europe still faces the challenge of an enormous amount of damaged wood. In Germany, a cold, wet summer helped to reduce the overall volume since the sad record year of 2020, when 73 million m³ had accumulated. Nonetheless, 43 million m³ of damaged wood were recorded in 2021. As a result of the calamity, the amount of available German spruce logs will halve by 2050.

Meanwhile, exports of big volumes of log wood to China continue. It is estimated that Germany shipped over 7 million m³ to China in 2021. Chinese log buyers are present in all European countries and they drive up prices at almost every log auction from France to Belarus.

Massive investments to be made

The money which Central European timber companies earned in previous years is invested:

- by 2023: (spruce) cutting to increase by 6 million m³ a year (Germany, Austria, Czech Republic, Slovakia)

- by 2023: CLT production up by 1.3 million m³ a year (1.6 million m³ in additional demand for lumber)

- by 2023: pellet production to increase by 350,000 tons in Austria and by 800,000 tons in Germany

- by 2023: six or seven additional production sites for wood fiber insulation boards

- by 2023: the world’s most modern wooden house productions (Blumer-Lehmann, b-solution, Gropyus, Kaufmann Bausysteme, Ziegler, ...)

Many changes, some constants in 2022

The following may apply as a short outlook for 2022: We are starting the new year with higher stock levels than twelve months ago. This year, demand will remain at least at the level recorded in 2021. The challenges in logistics will likely become bigger.

Hopefully, everyone in the timber industry has learned their lesson from 2021: Products are available in sufficient quantities, but they are often in the wrong place. Having one’s own warehouse and a little patience is better than to contact five producers in a panic.

Producers learned that the prices, which were paid for almost all wood products in 2021, would have been unthinkable before.