Forestry economically without a chance

In light of such low revenues, accompanied by higher costs for harvesting, silvicultural measures and the maintenance of machines and buildings, it has become impossible for forest owners to cover their expenses and, as a result, to generate sustainable profits in order to make the necessary investments for the reforestation of calamity-struck areas or for production-relevant restructuring processes without massive losses.

The winners of this development are big sawmills which also operate in transformation (especially cross-laminated timber). For years, these sawmills have been generating enormous added value due to the partial use of cheap damaged wood.

Cheap log wood increases sawmill profits

Even though sawmills, which do not operate in transformation, profit less, their revenue situation is still relatively positive. The cost structure of sawmills with up to 80% of raw material costs leads to enormous increases in revenue thanks to the reduction of log wood prices by 20% and of damaged wood prices by up to 50%. These increases are not passed on to “end consumers” by the timber and sawmill industry. In light of this situation, the author considers this practice of putting brutal pressure on softwood log prices unfair. In German speaking countries, this is mainly done by big sawmills.

Long-distance transport makes wood not ecological

It is the dilemma of the forestry sector that it profits when cutting capacities are too high in years when there is a lot of damaged wood. Sawmills, in turn, will continue to import considerable amounts of cheap log wood and put pressure on local forestry. Apparently, nobody cares about the environmental consequences. How sustainable can the renewable raw material wood be, when it is transported for hundreds of kilometers over several borders and past numerous sawmills, even though the buyer-sawmill is surrounded by forests?

Obviously, transport is way too cheap even when it comes to wood with its unfavorable weight-value ratio. Often enough, forest owners hear that log wood from the big calamity-struck areas of Central Europe is offered at a lower ex works price than when it’s offered free forest road near the buyer-sawmill.

Real and apparent profits

In this context, it is hard to understand the sales strategy of big forest owners who proudly mention high ex-works prices only to cart logs with freight costs of 25% of the wood price across three federal states past five bulk buyers. In the end, their profits, free forest road and exclusive of harvest costs, are minimal as well.

A balance between log cutting and consumption can be expected only in the long term, after the gradual replacement of fragile spruce forests and a prolonged period of time without vast calamities in Central Europe. Only then the forestry sector is going to be able to generate appropriate revenue again.

Until then, it will face very difficult times which are going to force many owners, who do not have proper sources of income, to give up.

Which company structures will survive?

One can assume that forest owners in climatically favorable locations, e.g. in the Alpine region where precipitation is frequent, are going to be able to maintain spruces to a relevant extent. In those regions, forestry with its traditional structures can survive. In other regions, forest owners are going to opt for plantation-like cultivation by planting conifers (various types of pines, Douglas fir) and fast-growing species – provided that they want to continue to operate in the forestry sector and that there are suitable locations (good credit standing) and altitudes (suitable for harvesters).

Forests “out of use” because of losses

Many forest owners, who have neither the capital nor the time or know-how for these massive changes, are not going to continue cultivating their forests. Some of them are going to try to survive economically by generating revenue through activities in other areas, such as the energy industry, tourism/recreation, forest burials, or public funds (premiums for discontinuing activities, nature conservation agreements).

Initially, the economically necessary termination of many forestry businesses might lead to positive changes in the eyes of environmentalists. Soon, however, the negative effects will manifest as well (decrease in traffic safety, no maintenance of roads and paths, deterioration of entire groups of trees of the same age etc.).

Intensive instead of multi-functional forestry

Without an economic perspective, a good part of forest owners is going to give up. Others are going to opt for intensive cultivation (full mechanization, shorter rotation periods, reduction of the number of trees) Worldwide, various pine species are most often used for construction purposes. These species facilitate the commercial production of wood even in more arid regions. Unless it is motivated by subsidies or forced by changes in the law, forestry in Central European forests, which are going to be mostly free of spruce by then, is going to focus even more on operational safety, cost cutting and optimization of yields.

Outside the Alps only wood from plantations?

One can assume that for this purpose, the goal is the fully mechanized work in stable forests with marketable and fast-growing tree species. However, these demands by ecologists are difficult to meet with mixed deciduous forests with a high number of old and dead trees or various types of so-called “potentially natural forests”.

Even though the weather-related damaged wood situation is going to lead to an even more one-sided “market power” of timber industries in the medium term, circumstances are going to change considerably in the long term. If it wants to profit from the increasing global demand for wood in the future, the Central European timber industry needs a reliable supply from predictable greater regions but not from international raw material markets. Worldwide, countries with a huge potential because of their size (South America, China) are carrying out extensive reforestation projects (rotation period < 40 years), not only to reduce soil erosion and greenhouse gas emissions, but also to still the growing hunger for wood.

Log wood from South America?

At the same time, softwood logging will decrease considerably in Central Europe because of the gradual disappearance of spruces. The question is: Is the timber and sawmill industry as a “market partner” going to give forest owners the possibilities and motivation for the reconstruction and production-relevant reforestation of calamity-struck areas? Or are the timber industry’s strategists (as a sort of inversion of log wood exports to insufficiently supplied China) thinking about importing softwood logs from South American plantations or relocating their businesses to forest regions outside Europe in 20 years?

Precisely because the “market partner” timber industry profits massively from this existence-threatening situation in which forest owners find themselves, it should rethink its repressive price policy.

You always meet twice in life

In the long term, there could be winners also in the forestry sector. The winners could be forest owners who successfully maintain stable forests with relevant percentages of spruces. Then the tables could turn. Spruces could become a scarce and highly sought after product again – and the forestry sector will remember the sawmill industry’s price policy during years which were difficult for forest owners.

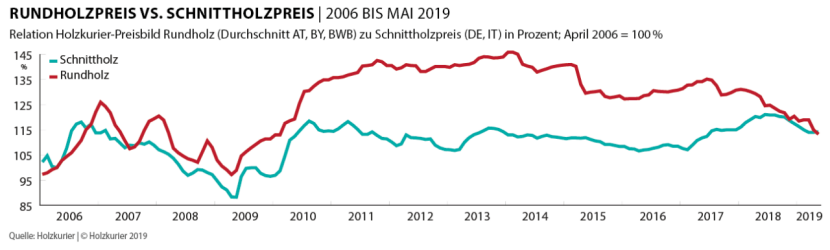

Log wood price vs. sawn timber price 2006 - May 2019

Relation of Holzkurier price picture for log wood (average of AT, BY, BWB) and sawn timber price (DE, IT) in percent; April 2006 = 100%; red: log wood, blue: sawn timber

© Holzkurier.com

Everybody is going to lose

Frank Diehl foresees a dramatic change in the Central European forestry industry where the cultivation of spruces will be limited to the Alpine region where there is more frequent precipitation. Outside this region there could be conifer plantations or forests which are “out of use”. In the long term, the sawmill industries, which now profit from the drop in log wood prices, are going to be on the losers’ side as well.

Facts and theses

- Drop in log wood prices due to an excess in supply in Austria (since 2015 > 40% damaged wood; log wood imports 2012-2018 from 6.0 to 9.1 million sm³ and a constant export of 0.8 million sm³)

- Enormous profits of the sawmill/timber industry (2015-2018) also due to discounts of up to 35 €/sm³ for Cx wood

- Unprofitable forestry: low revenues from timber sales (drop in prices and deterioration of assortments), higher costs for harvest, silvicultural measures and maintenance of forestry machines (additional burden because of untimely harvest/transport)

- Spruce as main species only in the Alpine region

- Plantation-like cultivation of conifers outside the Alpine region

- Ex-works prices can be misleading, when freight costs exceed 25% of the wood price free forest road

- Forests which are “out of use” offer fewer meta-economic possibilities

- The forestry sector will generate appropriate revenue only in the long term.

- Sawmills need softwood in the long term: Will it be imported from overseas plantations in the future?

- The timber industry needs to rethink its repressive price policy or continue to misjudge the repercussions.