© Holzkurier

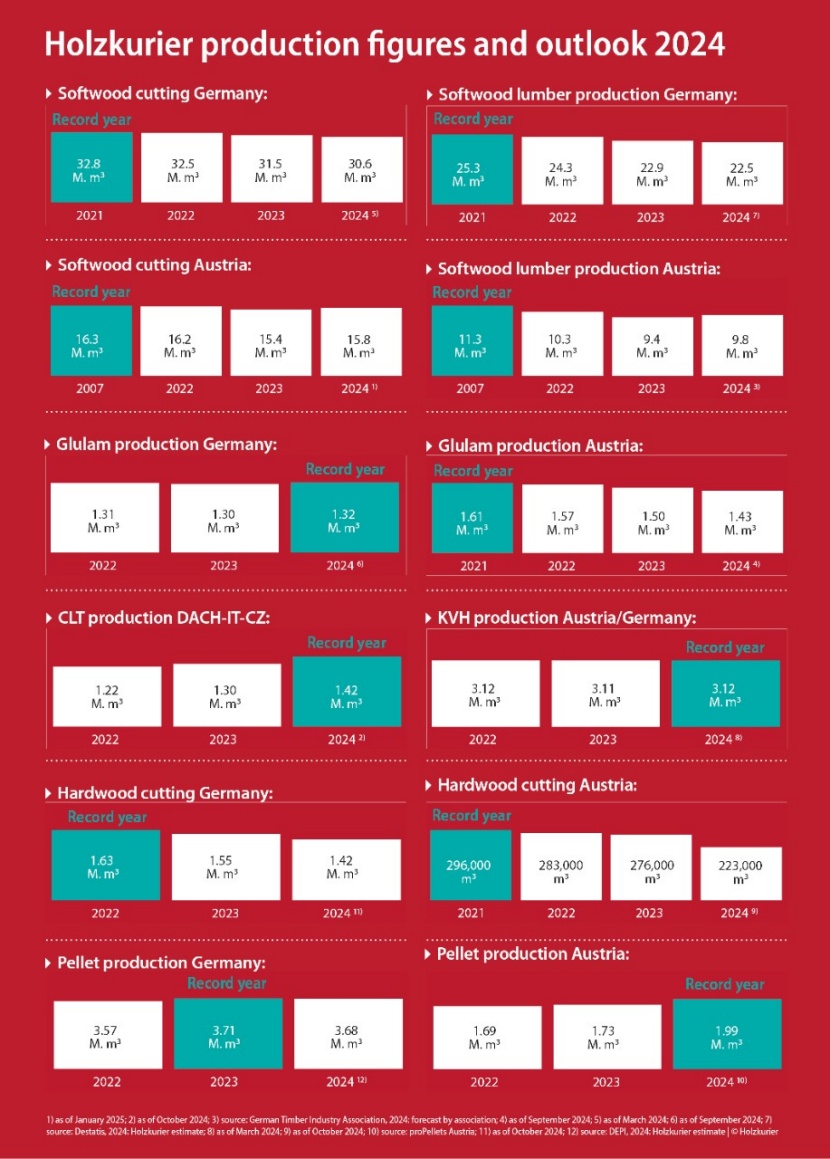

For cross-laminated timber, it was a record year – like every year since records began in 2008. Since CLT is basically produced to order only, it can be assumed that the additional volumes produced were also used for specific projects. Given the weak construction industry, this is a remarkable achievement, one that hardly any market participant celebrated, though. After all, it was not strong demand, but the massive increase in capacity in recent years that led to bigger volumes being constantly placed on the market, thereby keeping prices at a very low level. While the price indices for solid structural timber and glulam were around a quarter above pre-Covid levels (January 2019) at the turn of the year, CLT still fell 3 points short of the 100%-mark.

Glulam supply matched demand

Solid structural timber prices, too, were under strong pressure in 2024, with production volumes in Austria and Germany remaining constant at 3.12 million m³ for the third year in a row. At least that was the forecast of solid structural timber producers in the most recent production survey in spring 2024. Numerous conversations with market participants, in which the unexpectedly good capacity utilization at inadequate prices was repeatedly pointed out, indicate that the above-mentioned output was actually achieved.

As for glulam, supply and demand were much more balanced lately. Germany and Austria produced a total of 2.73 million m³, which corresponds to a slight decrease of around 1% compared to 2023. In Austria, production output was down by 4% to 1.43 million m³, and thus fell short of the record year of 2021 by about 11%. Germany, however, achieved its highest output of all times with an increase of 2% to 1.32 million m³.

Less lumber produced in Germany, more in Austria

Austrian softwood sawmills still hold by far the oldest production record in the Holzkurier statistics. The cutting of softwood logs was never at a higher level than in 2007, although this record was almost broken in 2022. A substantial decrease followed in 2023 and, most recently, a moderate increase of 2% to 15.75 million m³.

In Germany, on the other hand, the downward trend in the cutting of softwood logs continued for the third consecutive year, after having set a new record in 2021 at 32.77 million m³. Compared to 2023, cutting decreased by almost 3% in 2024 – and was thus 6.5% below the level of the record year.

In 2024, sawmills struggled with shrinking margins, with the increased cost of production and especially raw material prices as well as weak demand putting pressure on them. Across Europe, demand for softwood lumber decreased by a further 2 million m³ year on year to 65 million m³ in 2024. Compared to the record year of 2021, output has fallen by as many as 17 million m³, which corresponds to Austria’s cumulative production over the past seven quarters. As for this year, the European Sawmill Association expects a return to the 2023 level of 67 million m³.

Decrease in hardwood cutting

According to the Holzkurier’s survey, Austrian hardwood sawmills recorded the biggest decrease in hardwood cutting last year, with a drop of almost 20% to 223,000 m³. Abalon, the largest hardwood sawmill in the country, was the main reason for this development. The company, which was named “Sawmill of the Year 2025” by the Holzkurier, temporarily stopped production at its sites in Heiligenkreuz/AT and Schwalmstadt/DE and supplied its customers from pre-produced stocks. In addition to relieving the market, this groundbreaking strategic decision gave Abalon time to optimize processes and modernize the company, and employees some rest. In 2025, the company wants to slowly ramp up production again and then continue without any baggage from the past. If Abalon had continued production at the previous year’s level, hardwood cutting in Austria would have decreased by just 5%.

Abalon’s shutdown had a much smaller impact in Germany. There, hardwood cutting was down by 8% compared to 2023, totaling 1.42 million m³ in 2024. The two largest hardwood sawmills in Germany, i.e. Pollmeier Massivholz (840,000 m³) and Holzwerk Obermeier (100,000 m³), cut around the same volumes as in the previous year.

The hardwood sawmills are faced with major challenges, as was heard at the International Hardwood Conference in Vienna in November 2024, for example. Market participants attribute these to the difficult economic environment and increased wage and energy costs. So far, the majority of lower-quality lumber has been exported to China, but there is no longer a market for it. In addition, the parquet industry is under enormous pressure, also due to the sharp decrease in construction activity.

Record year for pellets

Due to the warm winter and the still full warehouses of end users, Austrian pellet producers got off to a very slow start in 2024, with the Italian market in particular being weak. “Over the course of the year, however, the filling of more than 20,000 new pellet storage facilities and warehouses and rising consumption in the commercial sector led to an increase in overall consumption and also boosted production,” Doris Stiksl, managing director of proPellets Austria, analyzes. The (preliminary) result is a remarkable 15% increase to 1.99 million tonnes of annual production in Austria.

No concrete 2024 production figures are available for Germany as yet. The DEPV expects the cumulative output to be slightly lower than the quantity of 3.8 million tonnes forecast in the spring of 2024. The reasons for this are the still high inventory levels due to overstocking, the warm winter of 2023/2024, and the slump in sales of new pellet heating systems. If the production volumes of the first three quarters are extrapolated to the entire year, the resulting quantity is 3.68 million tonnes, which is close to the record quantity of 3.71 million tonnes produced in 2023.