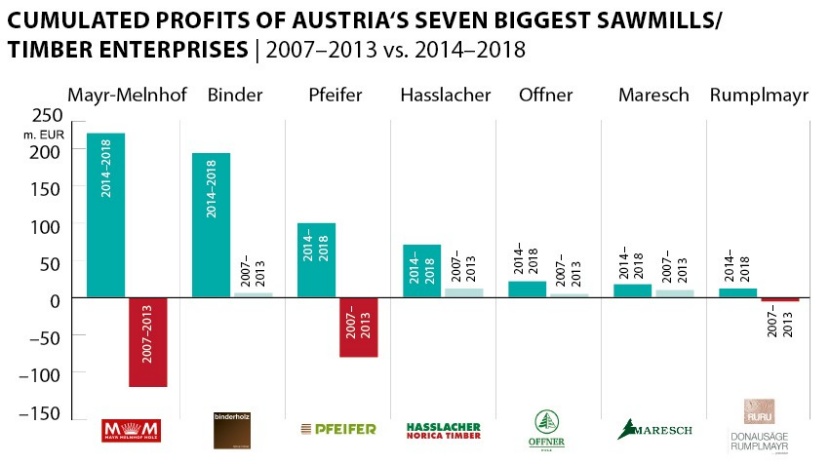

The headline of the 2015 balance sheet analysis for 2007-2013 was: asset erosion. The seven biggest Austrian sawing businesses had accumulated a loss of €137 million during that period. Hardly any investments were made, Austria's surplus logging capacity was officially claimed to be "more than 20%" - and instead of takeovers, there was only talk of shutdowns.

Situation has changed completely

Looking back at the past five years today, everything is completely different::

- The four biggest timber companies in Austria have massively bought themselves into business abroad. (In 2017, Binderholz took over Klenk Holz, Hasslacher incorporated Nordlam, Mayr-Melnhof Holz bought Hüttemann and Pfeifer Holz acquired Chanovice.)

- The biggest loss-maker (-€126 million) turned into the biggest profit earner (+€221 million): Mayr-Melnhof Holz.

- With Binderholz, Austria is now home to a new "Sales Croesus": €1 billion yielded in 2018 (+171% compared to 2013).

- The net equity base of those seven enterprises increased from 35% in 2013 to 47% last year. (In absolute figures, equity more than doubled from €451 million to €942 million.)

- Turnover increased from €1.8 bn. (2013) to €3.2 bn. last year.

- Material costs (essentially roundwood) amounted to €1.2 bn. in 2013, five years later the total was €1.7 bn.

All assessed enterprises continue to be family businesses. With the exception of Mary-Melnhof Holz, all of those companies are also owner-operated - this was already the case in the bright red years of 2007-2013.

Four fully integrated operations lead the way

The landscape also changed insofar as four timber companies have become sales kings by now. Binder (€1 bn), Pfeifer (€707 m), Mayr-Melnhof Holz (€684 m) and Hasslacher (€427 m).

The by far most dynamic timber enterprise in that period has been Binderholz: Their sales increased by 171%. Second place, which comes as no surprise, goes to Hasslacher Holding that generated 149% more turnover than in 2014. Both companies have long lists of acquisitions and investments.

On average, all seven companies had a sales increase of 72%. This makes those companies not only the biggest but also the most expansive enterprises of the whole sector. For comparison's sake: The entire Austrian wood industry yielded a turnover of €7.5 bn in 2013. In 2018, sales amounted to €8.33 bn - this is 11% more.

| 2014 | 2015 | 2016 | 2017 | 2018 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | |

| Sales | 1,945 | – | 2,007 | – | 2,190 | – | 2,448 | – | 3,168 | – |

| Material costs | 1,225 | 63 | 1,230 | 61.3 | 1,285 | 58.7 | 1,406 | 57.4 | 1,738 | 54.9 |

| Personnel costs | 239 | 12.3 | 251 | 12.5 | 279 | 12.7 | 318 | 13 | 404 | 12.8 |

| Write-offs | 87 | 4.5 | 91 | 4.5 | 105 | 4.8 | 113 | 4.6 | 128 | 4 |

| Result of ordinary activities | 37 | 1,9 | 80 | 4 | 159 | 7.3 | 177 | 7.2 | 330 | 10.4 |

| Surplus | 36 | 1,9 | 64 | 3.2 | 142 | 6.5 | 142 | 5.8 | 255 | 8 |

| Equity | 466 | 37.4 | 513 | 38.7 | 611 | 43.7 | 750 | 42.1 | 942 | 46.9 |

| Balance sheet total | 1,247 | – | 1,326 | – | 1,398 | – | 1,783 | – | 2,010 | – |

From restructuring to takeover

Source: Annual and consolidated financial statements © Timber-Online

The most conservative enterprise during this period of observation was Mayr-Melnhof Holz. Its sales "only" gained 22% between 2013 and 2018 (compared to the average of 72% of all seven companies). In light of the point of departure in 2013, this comparatively slower pace of growth is not surprising to CEO Richard Stralz. In 2014, banks approved the expansion of the CLT production in Gaishorn as one of the first measures. The restructuring was only officially completed in 2016. The real bombshell came in 2018 with the takeover of Hüttemann Holz. And more bombshells could follow: The company already announced a second CLT production site in Paskov or Leoben.

After the crisis years, the owners of several enterprises complained: "We have learned to generate better results with significantly less sales." As it turned out, there were not just empty words. The result of ordinary activities of the "Great Seven" totaled €11 million in 2013 - in 2018, it amounted to €330 million - a thirtyfold increase (note: EBT in the case of Mayr-Melnhof Holz).

| 2007–2013 | 2014–2018 |

|---|---|

| Sales increase of +45% of all seven enterprises | Sales increase of +163 % of all seven enterprises |

| €137 million of loss for all seven enterprises | €638 million of profits for all seven enterprises |

| Biggest losses: Mayr-Melnhof Holz with €126 million | Biggest profits: Mayr-Melnhof Holz with €221 million |

| Rank | Company | in million € |

|---|---|---|

| 1 | Binderholz | 128 |

| 2 | Mayr-Melnhof Holz1 | 75 |

| 3 | Pfeifer Holding | 62 |

| 4 | Hasslacher Holding | 31 |

| 5 | Holzindustrie Maresch | 14 |

| 6 | Offner Holzindustrie2 | 12 |

| 7 | Donausäge Rumplmayr | 8 |

| Rank | Company | in million € |

|---|---|---|

| 1 | Binderholz | 999 |

| 2 | Pfeifer Holding | 707 |

| 3 | Mayr-Melnhof Holz | 684 |

| 4 | Hasslacher Holding | 427 |

| 5 | Holzindustrie Maresch | 146 |

| 6 | Donausäge Rumplmayr | 105 |

| 7 | Offner Holzindustrie* | 100 |

Margin success is relative, others perform better

Source: Annual and consolidated financial statements © Timber-Online

Why was it that Austrian sawmills and further processors displayed such a successful performance between 2014 and 2018? "An EBITDA margin of 17% is actually not that good. The large state forest companies have similar cash flows, the paper and panel industries continuously register even better figures," Reinhard Binder, owner and managing director of Binderholz, puts the figures of 2018 into perspective (see article "Top year 2018").

Chance ...

Timber-Online price graphics © Timber-Online

In four of the five examined years, roundwood supply was suitable. And in at least three years of those, the actual roundwood price matched the level that sawmills themselves deemed appropriate (average spure/fir price southern Germany, Austria: 2014: €98/sm³, 2015: €92/sm³, 2016: €90/sm³, 2017: €92/sm³, 2018: €87/sm³, 2019 so far €77/sm³).

In parallel, opportunities opened up all over the world, and sales boomed. For the first time ever, demand increased on two gigantic overseas markets at the same time: USA and especially China. On top of the good results, the traditional markets (MENA region) were complemented by new sawn timber destinations: Pakistan, South Korea, Australia, India. Markets that in the past were virtually impossible to serve suddenly started buying. This acceleration in demand gave rise to increasing sawn timber prices. The average price in 2018 of softwood lumber assortments that are surveyed by Timber-Online was 25% above the level of 2008.

... and brains

Sawmills neither have direct influence on the selling conditions on global markets nor on roundwood supply. However, what is indeed in their power is the strategic development towards fully integrated plants. For this purpose, an extract from Binderholz's balance: "The internal further processing of the Binder group furthermore effectuated (in 2018) that the capacities of production units could be utilized throughout the entire year. The price level developed according to demand."

Furthermore, the for biggest timber enterprises are fully active in the cross-laminated timber business. Additionally considering Holzindustrie Offner and its subsidiary KLH, the top 5 benefitted from the growth in CLT demand between 2014 and 2018. The assessment by the Timber Online editorial department sees a demand increase of at least 60% during these five years.

Another fully integrated company

For comparability's sake, the analysis (2007-2013) of timber enterprise Johann Offner Holzindustrie again was evaluated without KLH. Together, the two company parts generated a turnover of about €171 million in 2018. The joint earnings before taxes amount to €14.6 million.

Balance sheet analysis: Austria 2014-2018

Method: Analogous to the Analysis of 2007–2013, the group balance sheets of Mayr-Melnhof Holz, the Pfeifer Group, Binderholz, Hasslacher Holding, Maresch Holzindustrie, Johann Offner Holzindustrie and Donausäge Rumplmayr were analyzed.

Selection criteria were a logging volume of at least 500,000 sm³/yr and company domicile in Austra (this is why Stora Ensa as well as the Schweighofer group - who is not operating any domestic sawmills - are missing in this list).

Company, domicile: Pfeifer Group, Imst; Binderholz, Fügen; Hasslacher Holding, Sachsenburg; Donausäge Rumplmayr, Altmünster; Offner Holzindustrie, Wolfsberg; Mayr-Melnhof Holz, Leoben; Holzindustrie Maresch, Retz.

Balance sheet analyses

„Top year 2018“ – Binderholz

Binderholz generated an EBITDA margin of 17% and €1 bn of sales last year.

„Richtung 700 Mio. €“ ("Towards €700 million" - article in German) – Mayr-Melnhof Holz

A sales plus of 24%, EBT plus of 34% and an annual surplus of 32% – this was the year of 2018 for the Mayr-Melnhof Holz Holding.

„Cashflow +32%“ (article in German) – Hasslacher Holding

The Hasslacher Holding boosted its sales to €427 million (+19%) last year. The consolidated profit gained 37% to €22.9 million.

„Unkonventionell erfolgreich“ ("Unconventionally succesful" - article in German) – Holzindustrie Maresch

The "equity Croesus" (continuously around 70% of the balance sheet total) also achieved good results in 2018.

„Planned growth in stages“ – Ante holz

„We have entered the cross-laminated timber production sector,“ announced Jürgen Ante in July.

End-of-the-year reviews

2014 was the "year of cleanup efforts". The Cordes group acquired the Rettenmeier group. Stora Enso shut down it Sollenau site in Austria, Binderholz the MDF production in Hallein. There were several bankruptcies (Kern, Holzwerke Stingl). Oskar Pfeifer made the appeal to "cease logging on a weekly basis".

2015 showed signs of an upswing. Still, there were further takeovers: The Stallinger brothers, for instance, repurchased their family sawmill. Holzindustrie Schweighofer acquired the Klausner plant in Kodersdorf/DE, the RZ sawmill in Wiesenau became insolvent. Storm "Niklas" felled 2.5 million sm³ in Bavaria.

Insolvencies, takeovers and restructurings were also characteristic for 2016, with the German Pellets bankruptcy (total claims: €427 million) leading the way. What is more: The Binderholz group took over Vapo Timber and with this the sawmills in Lieksa and Nurmes at the beginning of 2016.

2017 was a "year of records". Binderholz acquired Klenk Holz, Hasslacher bought Nordlam in the German city of Magdeburg. Finally, Mercer taking over the last remaining Klausner group plant marked the historical end of a sawmill era. Several storms felled a total of roughly 16 million sm³.

In 2018, Timber-Online headlined "Year of Investment". Several companies announced investments of over €10 million. With Labe Wood, a €100 million new sawmill construction in Czech Republic was announced. A number of new CLT construction projects became known. The total damaged wood volume in Central Europe amounted to about 70 million sm³.