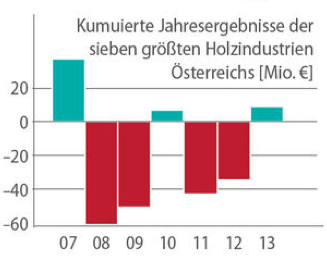

Accumulated annual profits/losses of the Top 7 of the Austrian sawmilling industry (in million euro)Source: annual reports © Timber-Online

Timber-Online analyzed annual reports of Austria’s seven largest sawmills and wood industries from 2007 to 2013. These are the main results:

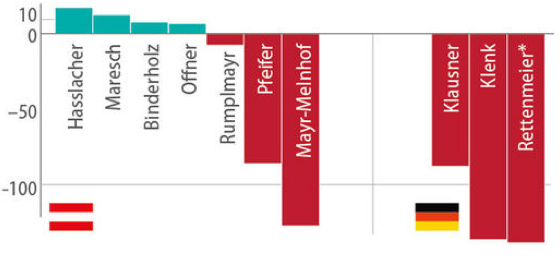

- Revenues have developed quite positively. On the basis of the published figures, they increased by 45% in the observation period At the same time, the industry amassed losses of 137 million The capital base shrunk by about a fifth on average The greatest loss made Mayr-Melnhof: 126 million. Now the sawmilling group with by far the highest sales in Austria has – on the basis of equity – slipped to 6th place

All family-owned companies

The study examined the consolidated balance sheets of Mayr-Melnhof, the Pfeifer Group, Binderholz, Hasslacher Norica Timber, the Holzindustrie Maresch, the Johann Offner Holzindustrie and the Donausäge Rumplmayr. The sample included all the groups with a minimum log input capacity of 500,000 sm³/yr which are headquartered in Austria. This is why the analysis did not consider Finnish-based Stora Enso and the Schweighofer Group which does not operate any sawmills in Austria. The companies in the sample are all softwood sawmills and still pursue that line of business. To begin with, the companies’ average values already reveal a clear picture of existing problems. Most of the analyzed companies also have locations both in Austria and abroad. So the figures discussed really reflect the situation in Central Europe. After all, all the companies are family-owned (apart from the fact that some loans were converted into mezzanine capital during restructuring).High losses

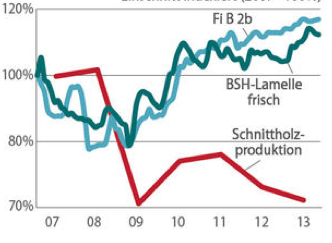

Trend of softwood log and lumber prices as well as indexed output (100%=2007)blue line: spruce logs graded Bgreen line: lumber for glulamsred line: lumber productionSource: Timber-Online, International Softwood Conference © Timber-Online

In terms of sales, the Austria’s leading companies are doing well. 2013 was the strongest year in the observation period (tied with 2011). Compared with 2012, revenues were up 3.6%. But what counts at the end of the year is not sales, but what is earned on it.

The crisis struck hard. 2008, 2009 as well as 2011 and 2012 were miserable years. During these years, losses of the seven companies accumulated to 190 million.

2010 (profits up 7.2 million) and 2013 (up 8.9 million) did offer respite, but without a chance to make up for the losses.

The majority of the losses of recent years were accumulated by the two groups with the highest revenues: Mayr-Melnhof (MM) and the Pfeifer Group. However, the financial development of these two could not be more diverse. During the financial crisis, MM’s equity dropped from 91.2 million to 20.1 million. The Pfeifer Group – despite six years of losses in a row – was proud to present 204 million of equity at the end of 2013. This is practically the same amount as the other six companies taken together.

Years without profit also in Austria

Accumulated annual results of Top 7 Austrian and selected German sawmills © Timber-Online

- In 2008, the export-oriented businesses were caught off guard by the economic crisis – even though inexpensive windthrow timber was readily available. The fact that lumber prices in Austria fell by relatively modest 15% did not help. Only three of the seven companies made it into the black. What remained at the end of the day were losses of 61.3 million. It was a very bad year also for Austria’s timber industry. 2009 was not much better, bringing losses of 50.7 million. The markets dimmed further. Lumber output slumped, as figures of the Austria’s association of the wood industry show. The Timber-Online survey showed the same decrease, but over a period of two years. An entire shift was omitted. Unfortunately, cuts were made only in production, not in the number of staff. In companies with sawmills as core businesses, the number of employees decreased by 15-20%. Companies with larger added-value productions found it even more difficult to adjust their workforce. Some of the processing capacities were significantly expanded. 2009 was also the year in which the roundwood prices embarked upon a multi-year period of bullish market. 2010 offered a chance to catch a breath. Production recovered slightly, lumber prices started to rise in the wake of roundwood prices. With the exception of the Pfeifer Group, leading businesses achieved marginal profits. The bottom line of the big seven was just 7.17 million. Yet whoever interpreted this as signs of recovery was proven wrong. Ever since 2011 at the latest, Central European sawmills were faced with the world's highest prices for roundwood. This reduces export earnings. At the same time, a gap between roundwood and sawn timber price trends opened. The industry slipped back into the red: -43.1 million. 2012 saw losses go down to "only" –34.9 million. But this is again deceptive as it is distorted by a 29.2 million sale-and-lease-back deal of Binderholz which was calculated as income from the disposal of fixed assets. When taking into account this device, overall losses amounted to 64 million which makes 2012 the worst year in the history of Austrian sawmill industry. 2013 might have been a silver lining, after all. Most companies were profitable again (or at least not negative). Combined profits increased to 8.9 million. Lumber production continued to fall under the influence of the ongoing crisis in Southern Europe and high roundwood prices. Yet the trend of price gaps somewhat closed again. Still only few businesses returned to a three-shift operation.