Source: Holzkurier market research © Timber-Online.net

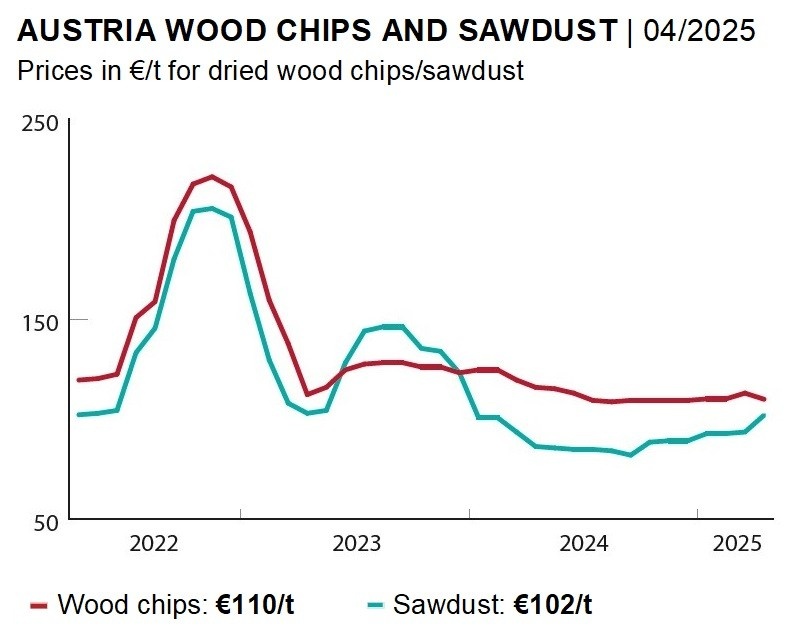

In the fourth quarter of 2024, prices for dried wood chips ranged from €100 to €115/t. In isolated cases, there are also reports of €120/t and more. However, these often apply to preliminary agreements with longer terms that were signed at the beginning of the year between individual Austrian pulp mills and large domestic sawmills. Back then, the purchasing mills considered these higher prices to be necessary due to the lack of deliveries from Germany, among other things. At the time, German sawmills had to curtail cutting either due to a shortage of log wood or because they were shut down as a result of insolvency proceedings, like Ziegler’s sawmill in Plößberg. In Germany, this is still reflected in higher wood chip prices compared to Austria.

The higher wood chip prices in Germany also played an important role in negotiations at the end of the quarter. According to the Austrian pulp industry, €105 to €115/t for dried wood chips are a competitive price level by international standards. Due to the recent increase in cutting, the outflow of wood chips was a focus of interest for the sawmill industry, so price extensions were also accepted.

Larger quantities of wood chips

So far this year, the sawmill industry has significantly increased its cutting volume. Last fall, many sawmills, especially in eastern Austria, were struggling with an insufficient supply of log wood. Over the course of the winter months, though, the situation has changed fundamentally. Little snow and dry soils have often made it possible to harvest log wood even at higher altitudes. Only in southern Austria have a few sawmills recently experienced shortages in log supply due to seasonal road closures.

Inventories at pulp mills still high

In the pulp industry, several companies have reported that their stock levels of both industrial log wood and wood chips will last them for more than six weeks. However, at least one pulp mill has already begun reducing its inventories during the first quarter, as extensive overhaul work is scheduled there in the fall. To make sure that there is sufficient storage capacity during the shutdown, purchasing has been restricted and supply quotas have been introduced early on.

Production activity at the six Austrian softwood-processing pulp mills remains at a relatively high level. In fact, there were no significant shutdowns or production curtailments during the first quarter, and shutdown measures are not planned for the second quarter either.

Narrowing gap between sawdust and wood chip prices

Unlike wood chips, negotiations on preliminary contracts for deliveries of sawdust have proven more difficult in the second quarter. Similar to the first quarter, there is competition over sawdust, primarily due to improved pellet production. As of the beginning of April, almost all Austrian pellet mills – both integrated and non-integrated ones – are operating at full capacity. Production levels are expected to remain high in the coming weeks as many end customers are currently stocking up on pellets.

However, sawdust was fought over not only due to pellet production. A comparatively large quantity was also exported to Germany. In the negotiations, sawmills were therefore able to charge pellet mills higher prices, as the latter had feared a supply shortage, especially at the time of the negotiations. As a result, some pellet manufacturers are paying over €120/t ex-sawmill for dried sawdust in the second quarter. The majority of contracts for dried spruce sawdust requested by pellet mills involve around €110/t ex-sawmill. Increases of €5 to €10/t to a price level of €100 to €105/t had already been implemented in the first quarter.

Not least due to these price demands, at least one manufacturer of wood-based materials has virtually abandoned the use of sawdust. Other panel factories have at least partially accepted the price increases. However, panel factories are willing to pay €90/t ex-sawmill even for freight-related quantities. In the east, the maximum is €100/t ex-sawmill for dried sawdust.

Board factories have increased production

The capacity utilization of the plants in use at the six chipboard production sites has increased substantially in many cases. MDF production at the only Austrian line has also gone up significantly.

However, it is currently expected that capacity utilization in pellet production, and thus demand for sawdust, will decrease again during the second quarter once end customers have completed the stockpiling. Although sawdust prices have been agreed for the entire second quarter, reductions before the end of June cannot be ruled out.