In 2021, the economic conditions could not have been more favorable for the timber industry, thanks to the interplay of the following factors:

- Low stock levels of almost all wood products in the first few months;

- A global boom, supply panic and speculative purchasing helped to make defensive prices accepted market prices that were outdated only a few weeks later.

These developments helped the Austrian timber companies to great operating results in 2021, which are now finally available. The balance sheets for 2022 have not been published yet but it is already safe to say that last year was significantly weaker.

Double-digit growth in revenue from ordinary activities

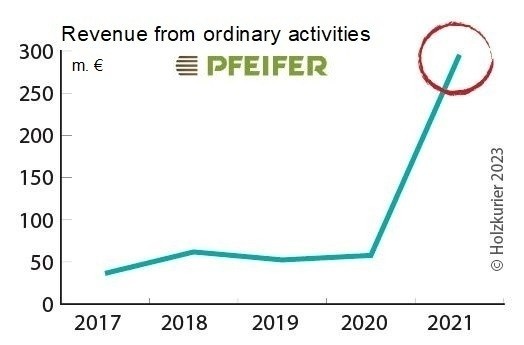

Pfeifer Group recorded the biggest increase in revenue from ordinary activities in 2021 © Timber-Online.net

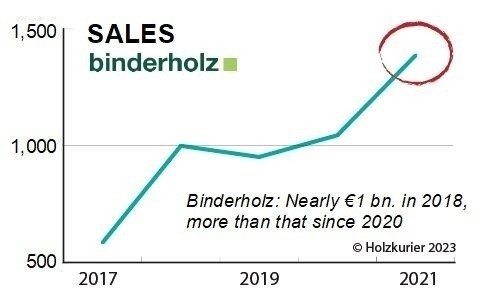

All six companies, which were considered for the balance sheet analysis, recorded double-digit increases in their respective revenue from ordinary activities (Mayr-Melnhof Holz and Binderholz use EBT, or earnings before taxes, instead). Within one year, Binderholz doubled its revenue from ordinary activities (+€232 million), bringing the total to €446 million. Pfeifer Holz even recorded a nearly fivefold increase to over €295 million.

Source: annual and group reports © Timber-Online

MM with special effects

In terms of revenue from ordinary activities, Mayr-Melnhof Holz saw the weakest growth in 2021, with +45% to €131 million. One explanation may be that the company was in the middle of putting together the balance sheet for 2021 when the war in Ukraine started, and had to react to these developments. “Other provisions” increased by around €40 million compared to 2020. As CEO Richard Stralz explains, “these provisions are aimed at cushioning the risk for the Russian plant as a result of the Ukraine war.” Without these provisions for impending losses, Mayr-Melnhof Holz’s EBT or revenue from ordinary activities would have been higher – and the company would have doubled its result.

All financial figures were outstanding

No matter which financial key figure you look at, there was growth everywhere in 2021. All six timber companies saw their sales increase by double digits and, at an average of 25%, operating margins were outstanding as well.

Binderholz is in a league of its own with an operating margin of over 30%. Mayr-Melnhof Holz had the smallest operating margin in 2021, i.e. 16%. In normal years and over the course of sawmill history, this would have been considered an “extremely good” margin.

Source: annual and group reports © Timber-Online

| Company | in million € | Diff. in % |

|---|---|---|

| Binderholz | 446 | +109 |

| Pfeifer Group | 295 | +412 |

| Mayr-Melnhof Holz | 131 | +45 |

| Hasslacher Holding | 108 | +225 |

| Holzindustrie Maresch | 64 | +94 |

| Johann Offner Holzindustrie | 37 | +236 |

| Company | in million € | Diff. in % |

|---|---|---|

| Binderholz | 1,387 | +33 |

| Pfeifer Group | 1,012 | +51 |

| Mayr-Melnhof Holz | 806 | +28 |

| Hasslacher Holding | 606 | +41 |

| Holzindustrie Maresch | 222 | +53 |

| Johann Offner Holzindustrie | 137 | +62 |

| Company | in % |

|---|---|

| Binderholz | 32 |

| Pfeifer Group | 29 |

| Holzindustrie Maresch | 29 |

| Johann Offner Holzindustrie | 27 |

| Hasslacher Holding | 18 |

| Mayr-Melnhof Holz | 16 |

| 2019 | 2020 | 2021 |

||||

|---|---|---|---|---|---|---|

| in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | |

| Sales | 2,963 | – | 3,001 | – | 4,169 | – |

| Material costs | 1,460 | 49.3 | 1,347 | 44.9 | 1,883 | 45.2 |

| Staff costs | 426 | 14.4 | 434 | 14.5 | 470 | 11.3 |

| Amortizations | 140 | 4.7 | 153 | 5.1 | 181 | 4.3 |

| Revenue from ordinary activities | 360 | 12.1 | 439 | 14.6 | 1,081 | 25.9 |

| Surplus | 290 | 9.8 | 328 | 10.9 | 814 | 19.5 |

| Equity ratio | 1,126 | 55.3 | 1,362 | 59.6 | 2,058 | 49.4 |

| Balance sheet total | 2,035 | – | 2,287 | – | 3,261 | – |

Growth at a peak in 2021

For all companies, 2021 was the culmination of the ten-year period of growth which started in 2012.

This ten-year long upswing is all the more remarkable because of how it started: In 2012, the six timber industries had accumulated losses of €67 million. In 2021, on the other hand, there was a surplus of €814 million (+148% compared to 2020).

Business done more effectively

From 2012 to 2021, the analyzed companies became more profitable and more effective in doing business. The companies’ equity ratios have also increased, indicating healthy growth. In these ten years, sales increased by a factor of 2.4, from €1.8 billion in 2012 to €4.2 billion in 2021.

The timber companies have significantly bigger assets than they used to, as the balance sheet total shows. In 2012, assets had totaled €1.3 billion. Ten years later, they were already close to €3.3 billion. The expansion into Germany (Pfeifer Holz, Binderholz, Hasslacher Holding, Mayr-Melnhof Holz), the Czech Republic (Holzindustrie Maresch, Pfeifer Group) as well as the US and Finland (Binderholz) is well known.

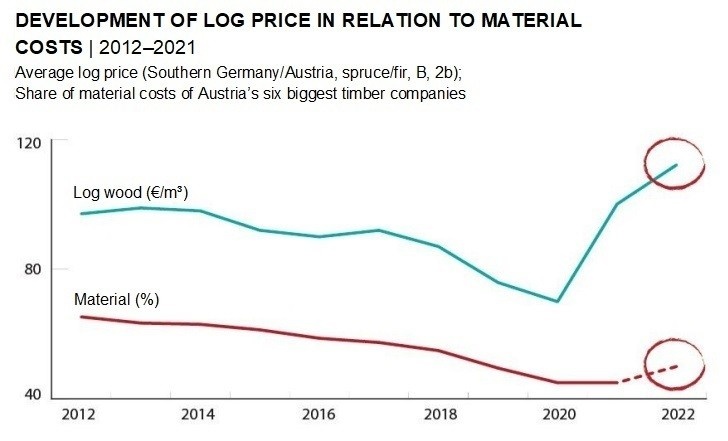

Material costs affected by damaged wood

Material costs, i.e. the cost of procuring log wood and other materials, rose steadily from 2012 to 2017 before falling again from 2018 to 2020 as a result of the damaged wood calamity. In 2021, material costs remained stable. Staff costs and depreciation have increased year after year, which also underlines the expansion of the companies.

One company stands out

© Timber-Online

In terms of growth, Binderholz is in a league of its own. The family dynasty from Tyrol has seen a consistently positive development since 2012. In the ten years to 2021, net profit increased by 1,129%. 2017 (acquisition of Klenk Holz), 2018 and 2021 (first year after takeovers in the US) were particularly strong years in that respect. In 2018, Binderholz achieved a 71% increase in sales within just one year and was already close to the €1 billion-mark (2018: €999.499 million in sales).

Mayr-Melnhof Holz also recorded a positive development, interrupted, however, by larger fluctuations. In 2016, Pfeifer Group from Tyrol saw its net profit grow strongly, i.e. by 1,705.5%, and the following years were also characterized by growth. Hasslacher Holding managed to increase its net profit by 1,733.3% in the period from 2012 to 2021.

It is noticeable that the Pfeifer Group recorded a slump in earnings of -115.0% in 2015. That year, the balance sheet was even negative. Already in the following year, however, it was clearly positive again. Overall, these four Austrian companies show a positive development, with Binderholz and Hasslacher recording the strongest increases in annual surplus.

Share of material costs unchanged in 2021

In 2021, the share of material costs of Austria’s six biggest timber companies rose slightly to 45.2% (2020: 44.9%).

By July 2021, the log price had reached around €115/m³ in Southern Germany and Austria. Nevertheless, the prices of finished products saw an even bigger increase.

The timber companies have become increasingly integrated and cut log wood into lumber, which they then use for further processing. Ideally, the sawmill by-products are also processed in-house.

In 2019, material costs of the six timber industries accounted for 50%, compared to 60% in previous years. As for 2022, Holzkurier’s editorial team again expects a percentage of 50%.

© Timber-Online

Analysis of corporate balance sheets in Austria in 2021

In the past ten years, the balance sheets and annual reports of Mayr-Melnhof Holz, Pfeifer Group, Binderholz, Hasslacher Holding, Maresch Holzindustrie, Johann Offner Holzindustrie and Donausäge Rumplmayr were analyzed.

Selection criteria were an annual cutting volume of at least 500,000 m³ and headquarters in Austria. (This is why Stora Enso and HS Timber Group are not part of this analysis; they do not operate sawmills in Austria.) Starting this year, the Holzkurier will focus on only six companies: Pfeifer Group, Imst; Binderholz, Fügen; Hasslacher Holding, Sachsenburg; Offner Holzindustrie, Wolfsberg; Mayr-Melnhof Holz, Leoben; Holzindustrie Maresch, Retz.

In the case of Johann Offner Holzindustrie, KLH is not taken into account. The figures presented in this analysis are therefore purely sawmill figures. The same is true for Maresch Holzindustrie. The remaining four are fully integrated timber companies which operate production sites at an international level.

From “too good” and “good” straight to “very bad”?

© Holzkurier

2021 was such a positive year for Central European sawmills and timber companies that the Holzkurier dubbed it the “year of the century”.

2022, however, will likely see a return to more normal margins. The “Holzwurm” predicts a level similar to that of 2019.

In 2023, the world has fundamentally changed. Demand is currently similar to a normal pre-Covid year, log prices could reach record levels, while the prices for lumber and processed wood products have partly fallen by 60%. Log wood is not only more expensive than it was in 2021, it is also scarce in some regions. Demand on important sales markets in Europe and overseas is much lower.

At the beginning of 2023, some figures were in the red again. Everyone along the value chain should contribute to changing that. A year like 2021 does not have to and will likely not see a revival – but 2012 with its negative results must not happen either.

Otherwise, the financial resources would not be sufficient to seize the once-in-a-century opportunity for modern, liquid companies of using timber construction to tackle climate change.