Remarkable year

In October 2020, the International Softwood Conference started with the words: “This is a year we will never forget.” At the time, no one knew that 2020 would be followed by a historic year which would make all previous price levels seem obsolete.

Driven by a great price development in the US and very strong demand, lumber prices increased month after month starting in August. In the US, lumber suddenly fetched prices which were higher than those of highly processed glue-laminated timber. As a result, the “miracle product CLT” suddenly became something of a “problem product”.

Selling like hot cakes

In the fourth quarter of 2020, demand was so high that the timber companies were unable to stock up on wood before winter. This unique situation then led to the record year 2021.

Depending on their market positioning, the companies were able to profit from the general situation. However, of the seven companies only the two Tyrolean timber companies Binderholz and Pfeifer Holding managed to perform even better than in the great year 2019 when it comes to revenue from ordinary activities.

High-flyers off to even greater heights

© holzkurier.com

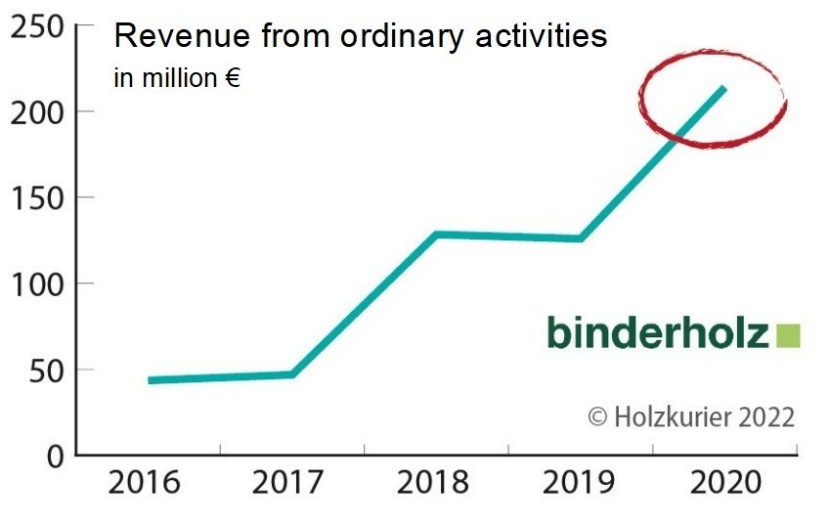

In 2020, Binderholz, the high-flyer of the past years, was once again the unrivaled number one in terms of performance. The company’s revenue from ordinary activities rose by 70% to €214 million in 2020. The gap to the other timber companies widened as well, from €40 million in 2019 to over €120 million in fiscal year 2020. Mayr-Melnhof Holz follows in second place with €90.4 million (-1%) in revenue from ordinary activities. The Styrian timber company thus managed to equal the record result of 2019. Pfeifer Holz is in third place with €58 million (+10%) and Hasslacher Holding ranks fourth with €33 million.

Billion-euro mark passed

© holzkurier.com

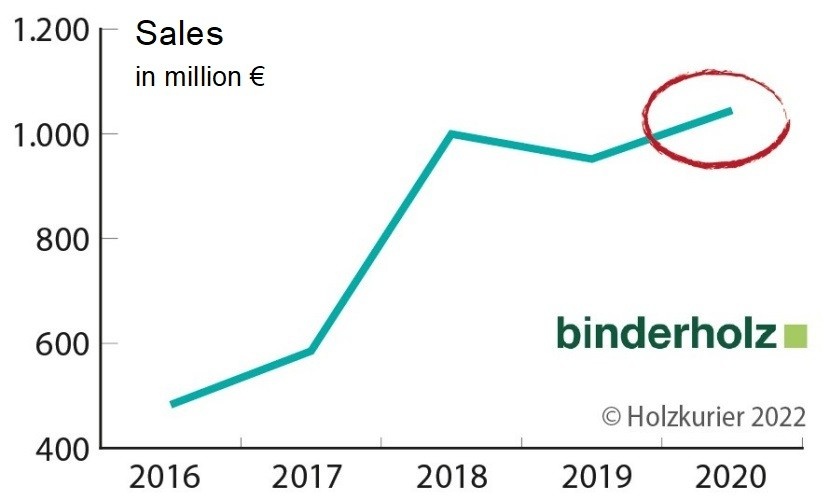

In 2020, there was a general downward trend in sales. The cheap log wood kept lumber prices at a low level over the entire year. Once again, Binderholz was the only exception. With a 10% increase in sales, Binderholz was the first German-speaking timber company to pass the €1 billion mark. As of mid-May 2022, the 2020 sales figures are already yesterday’s news, though. In 2021, Binderholz bought the two US sawmills from Klausner. Then, in January 2022, the closing for the acquisition of BSW took place. This year, Binderholz will become Europe’s biggest group in the segment of the sawmill and solid timber processing industry with total annual sales of over €2.6 billion and around 5000 employees.

Mayr-Melnhof Holz acquired three Swedish sawmills shortly before Christmas 2021, which will likely result in €265 million in additional sales. As a result, Mayr-Melnhof Holz could be the second company to exceed the €1 billion sales mark in 2022, after Binderholz.

Tenfold increase in revenue from ordinary activities since 2014

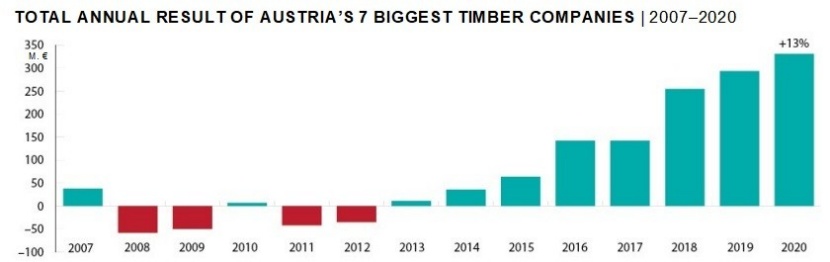

From 2014 to 2020, total sales generated by Austria’s seven biggest timber companies grew by 60%, from €1.9 billion to €3.1 billion – and another significant jump is expected by the end of 2022. For comparison: In terms of revenue from ordinary activities, the companies recorded a more than tenfold increase from €37 million in 2014 to €443 million in 2020. After this upward trend, the average equity ratio is 59%. Hasslacher Holding has the lowest equity ratio of over 40% after a massive investment program involving all of the company’s production sites.

© holzkurier.com

© holzkurier.com

| Company | in million € | Diff. |

|---|---|---|

| Binderholz | 213.8 | +70 % |

| Mayr-Melnhof Holz (EBT) | 90.4 | –1 % |

| Pfeifer Holding | 57.8 | +9 % |

| Hasslacher Holding | 33.3 | –17 % |

| Holzindustrie Maresch | 32.8 | –9 % |

| Johann Offner Holzindustrie | 11 | –25 % |

| Donausäge Rumplmayr | 3.9 | –29 % |

| Company | in million € | Diff. |

|---|---|---|

| Binderholz | 1,044 | +10 % |

| Pfeifer Holding | 669 | +1 % |

| Mayr-Melnhof Holz | 628 | –6 % |

| Hasslacher Holding | 430 | ±0 % |

| Holzindustrie Maresch | 145 | –5 % |

| Donausäge Rumplmayr | 85 | –5 % |

| Johann Offner Holzindustrie | 85 | –11 % |

| Company | in million € |

|---|---|

| Holzindustrie Maresch | 23 % |

| Binderholz | 20 % |

| Mayr-Melnhof Holz | 14 % |

| Johann Offner Holzindustrie | 13 % |

| Pfeifer Holding | 9 % |

| Hasslacher Holding | 8 % |

| Donausäge Rumplmayr | 5 % |

| 2016 | 2017 | 2018 | 2019 | 2020 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | in million € | in % of sales | |

| Sales | 2,190 | – | 2,448 | – | 3,168 | – | 3,052 | – | 3,086 | – |

| Material costs | 1,285 | 58.7 | 1,406 | 57.4 | 1,738 | 54.9 | 1,510 | 49.5 | 1,390 | 45 |

| Staff costs | 279 | 12.7 | 318 | 13 | 404 | 12.8 | 436 | 14.3 | 445 | 14.4 |

| Amortizations | 105 | 4.8 | 113 | 4.6 | 128 | 4 | 144 | 4.7 | 157 | 5.1 |

| Revenue from ordinary activities | 159 | 7.3 | 177 | 7.2 | 330 | 10.4 | 366 | 12 | 443 | 14.4 |

| Surplus | 142 | 6.5 | 142 | 5.8 | 255 | 8 | 294 | 9.6 | 331 | 10.7 |

| Equity ratio | 611 | 43.7 | 750 | 42.1 | 942 | 46.9 | 1,161 | 54.7 | 1,397 | 58.6 |

| Balance sheet total | 1,398 | – | 1,783 | – | 2,010 | – | 2,121 | – | 2,382 | – |

| 2007–2013 | 2014–2020 |

|---|---|

| 45% increase in sales for all seven companies in the years 2007 to 2013 | 59% increase in sales for all seven companies in the years 2007 to 2013 |

| €137 million in losses for all seven companies | €1.3 billion in profits for all seven companies |

| Biggest losses: Mayr-Melnhof Holz with €126 million | Biggest profits: Binderholz with €453 million, followed by Mayr-Melnhof Holz with €370 million |

Analysis of corporate balance sheets in Austria 2014–2020

*Method: As in the analysis of the years 2007–2013, the balance sheets and annual reports of Mayr-Melnhof Holz, Pfeifer Group, Binderholz, Hasslacher Holding, Maresch Holzindustrie, Johann Offner Holzindustrie and Donausäge Rumplmayr were analyzed.

The selection criteria were a cutting volume of at least 500,000 m³ a year and headquarters in Austria. This is why Stora Enso and HS Timber Group are not part of this analysis (they do not operate sawmills in Austria).

Company, headquarters: Pfeifer Group, Imst; Binderholz, Fügen; Hasslacher Holding, Sachsenburg; Donausäge Rumplmayr, Altmünster; Offner Holzindustrie, Wolfsberg; Mayr-Melnhof Holz, Leoben; Holzindustrie Maresch, Retz