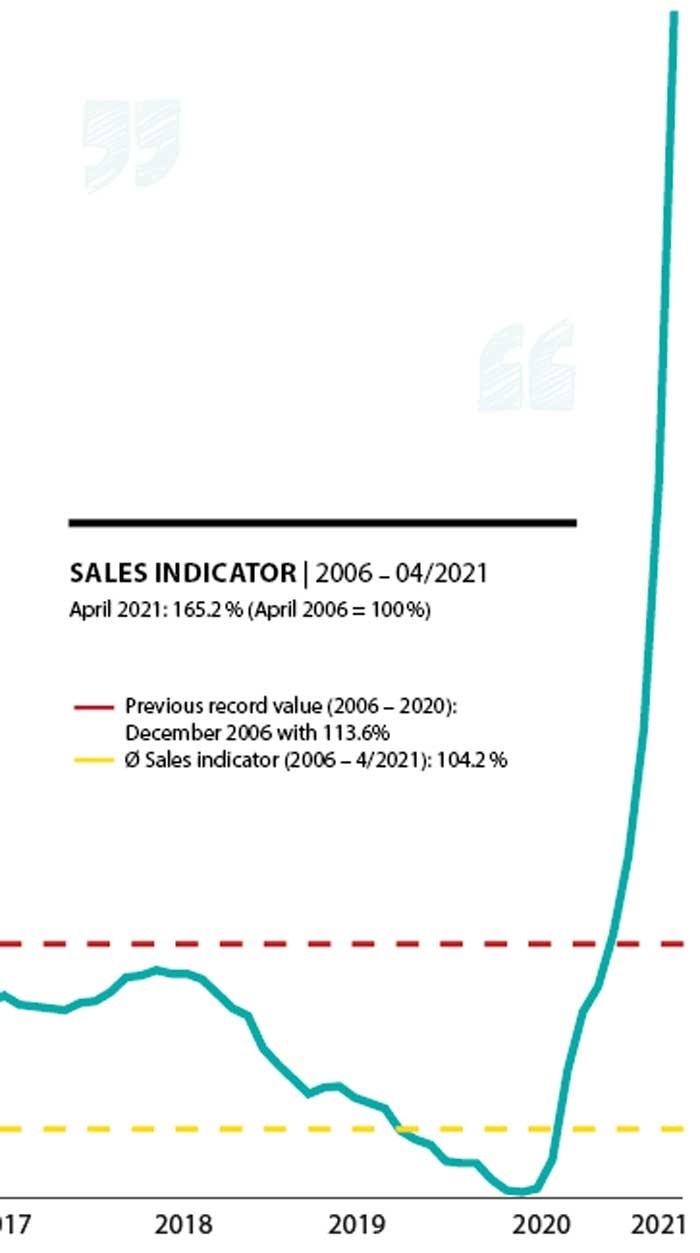

Sales indicator April 2021: Outside the usual range of fluctuations © holzkurier.com

With 165.2%, i.e. an increase of almost 26% compared to March, another preliminary record was reached which will be dated already in May, since current sales are often made already for June. Also, from today’s perspective, there is no lumber or processed product in Central Europe which will become cheaper by then.

It is not just the prices which are unique – the market is also out of joint in many respects: The market’s usual price relations are partly gone. In this context, the relation between log wood and lumber must be mentioned first of all. Log prices have seen a constant increase since July 2020. However, prices of lumber and processed products are rising much more sharply.

Price times four

The US softwood lumber price has seen the biggest increase. At the end of April, it reached €760/m³ which is quadruple the price recorded last year. With €664/m³, the average April price is twice the average value since 2006.

It has become hard to find the right adjectives to describe these prices. “Historic” can be used for April because they are not even remotely comparable with the past.

Twice the “normal” value

According to a survey conducted in Germany, numerous product groups which are used for pallets, boxes and cable drums are only available in very limited quantities. In Italy, 17 mm sideboards already came close to the €300 mark. Prices currently range from €240 to €300/m³ (free border). This is 2.2 times the price recorded last year. And the current price is also exactly twice the mean value of the years 2006–2021.

Substantial discrepancies

Packaging companies have to accept the highest price increases. At the same time, they cannot rely on a sufficient lumber supply. In France and Spain, these products are also scarce. There is currently a difference of almost €100/m³ between the lowest and highest prices.

Numerous packaging companies do not (or cannot) buy anything anymore. Italian customers who need special products, like 22 x 47 laths, find themselves in a similarly difficult situation. After decades, this product is no longer produced.

€300 €/m³ is also the price demanded by local sawmills for lumber which is shipped to the MENA region. North African demand is expected to be weak until the end of Ramadan. However, it is rather unlikely that larger quantities will be ordered for €330 or €340/m³ then. Big timber companies also “assigned” the assortments required for North Africa to other markets. And short-term sales are currently few and far between.

All of the big Central European companies are directly or indirectly active in the US. In their opinion, European prices will continue to rise until they have reached some sort of equilibrium. At the moment, prices are still several hundred euros per cubic meter away from it.

This* has never happened before!

- Lumber-log wood price ratio 2.6 times bigger than normal

- Currently reported prices often already refer to Q3.

- Roof laths cost up to €1000/m³.

- Price discrepancies of up to €100/m³ depending on the type of softwood lumber

- The US softwood lumber price has already reached €760/m³.

- The US price has quadrupled compared to last year.

- US lumber is €200/m³ more expensive than glulam in Europe.

- Glue-laminated timber (glulam) is more expensive than cross-laminated timber (CLT). Up until now, CLT was always around €150/m³ more expensive.

- Those who sell their goods at too cheap a price have their shelves picked clean.

- Monthly price increases of €100/m³

- “Daily prices” for packaging wood

- Offer with delivery volume and date: non-binding prices

- The OSB price rose from €180 to over €500/m³ within 12 months.

- New price lists at ever shorter intervals

- Customer: “I need one package, but I’ll order four because nothing arrives anyway.”

- Special lumber assortments are partly not even produced anymore.

- “We won’t give any quotations anymore.”

* List is not exhaustive