France and Italy hit hard

Host Keith Fryer (above), EOS president Sampsa Auvinen (bottom left) and ETTF vice-president Morten Bergsten greeted the online participants © Holzkurier.com

In March, the French and Italian construction sectors recorded contractions of more than 60%, while other countries, such as Germany, came though this period with a nearly stable development. This year, France’s softwood sawn timber demand is going to reach around 8.2 million m³. As for 2021, a 3% increase is expected. Bergsten puts Italy’s demand at 4 million m³ this year, with imports remaining constant at 3.8 million m³. In 2021, demand is expected to rise slightly. In this context, Bergsten mentioned the “Superbonus 110%”, a stimulus program for the construction sector introduced by the Italian government which gives building contractors tax benefits.

Germany’s softwood sawn timber demand amounts to 19.5 million m³ this year. Even though the construction sector is going to be slightly weaker in 2021, wood consumption is to remain unchanged according to Bergsten. His analysis of the British market was less positive. British imports are going to see an 11% decrease this year, followed by a 4% recovery in 2021. However, the ETTF estimates softwood sawn timber demand to be 10% higher next year.

Growing demand in 2020 and 2021

In 2021, the EU’s overall softwood sawn timber demand could increase by 2.3 million m³. When adding North America, overall consumption is going to rise by 11.1 million m³.

2021 brings a lot of uncertainties. The outlook for the timber industry is positive, though.

Remodeling one’s own four walls

This year, some trends emerged as a result of COVID-19 and they could continue in 2021, according to Sampsa Auvinen, President of the European Organization of the Sawmill Industry:

- people stay at home more and buy online (strong DIY and packaging segments)

- relocations to rural areas (boost for the DIY segment)

- increasing risk avoidance (home renovations stronger than new constructions)

- people spend less time in the office (increase in digitalization, fewer offices)

- construction activity is slightly decreasing

Central Europe at an advantage

Auvinen talked about the divided supply situation with Central Europe on the one hand where big volumes of damaged wood are accumulating in 2020 as well. In the north of Europe and in the Baltic states, on the other hand, the supply situation is much less good. Auvinen sees a slightly decreasing availability of log wood throughout Europe this year and in 2021. In the short term, Central European timber companies are going to maintain the competitive edge which they gained thanks to the raw material price. In Scandinavia, Sweden can hold its position on the market thanks to the currency devaluation – a possibility which Finland and the Baltic states do not have.

I was wrong last year when I said: ‘More is impossible.’ 2020 brings us record profits despite a 3% decrease in production. The numbers could continue to rise if US prices remain high. In this case, however, we will soon have a supply problem in Europe. Many customers are already complaining about not receiving enough sawn timber.

Higher overseas market shares

European sawn timber is going to gain further market shares on overseas markets in 2021. European exports to China and the US are reaching unprecedented levels. Japan and the Middle East are buying constant volumes of European sawn timber. As for the coming months, Auvinen expects softwood sawn timber prices and export volumes to continue to increase, while stock levels are going to decrease further.

Log wood as crucial element of success

© Holzkurier

For the medium-term outlook, Auvinen drew on Holzkurier’s survey on new construction projects. For him, the question was whether there is going to be enough raw material for all of those production capacities. “Regions, which do not have cheap log wood at the moment, could be among the winners. Last year I said: ‘More than this year is impossible.’ This year, though, we see new record despite a 3% decrease in production. The numbers could continue to rise if US prices remain high. In this case, however, we will soon have a supply problem in Europe.”

Market trends

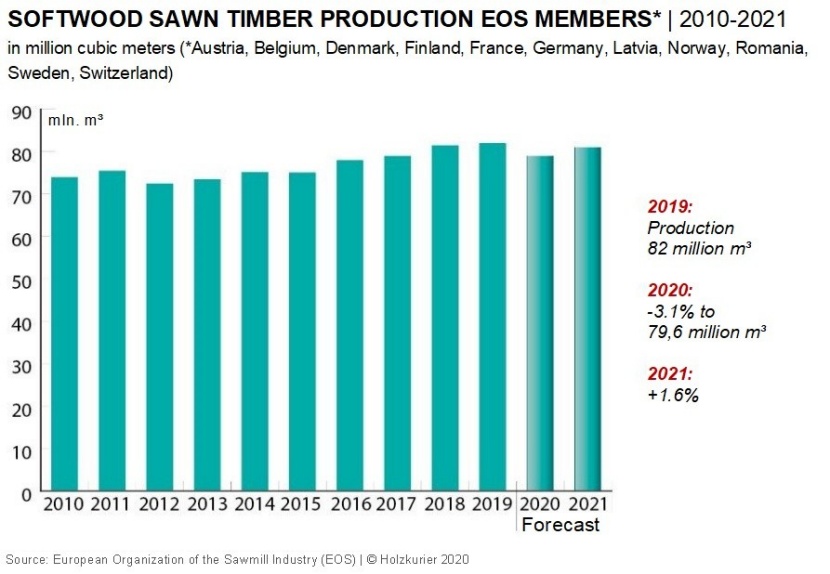

- Only slight decrease in EU demand in 2020 (positive development of DIY segment)

- Increase of 2.3 million m³ in EU’s softwood sawn timber demand in 2021

- Overall consumption in Europe and North America up by 11.1 million m³ in 2021

- Most countries predict an increase in demand in 2021 (stable construction activity)

- Italy: imports unchanged at 3.8 million m³ in 2020; consumption at 4 million m³; slight increase expected for both in 2021

- France: imports -12% this year (2021: +4%); consumption at 8.2 million m³ (2021: +3%)

- Germany: imports -2% this year (2021: unchanged); consumption at 19.5 million m³ (2021: unchanged)

- Great Britain: imports -11% this year (2021: +4%); consumption at 8.5 million m³ (2021: 9.5%)

TOP 4 COUNTRIES

#1 GERMANY

- Increase in softwood sawn timber production in 2020 and again in 2021 to nearly 25 million m³ a year

- Fourth year with big volumes of damaged wood

- Construction activity remained at a high level during corona crisis, therefore very stable domestic demand

- Recovery of other segments of the timber industry as well

- Booming exports: USA and China compensate for weaker markets elsewhere

#2 SWEDEN

- Decrease in softwood sawn timber production of around 500,000 m³ to 18.2 million m³ in 2020, and to 18.1 million m³ in 2021

- Production decreased due to repercussions of the pandemic despite strong demand

- Exports strong so far; China (+60% in H1) and the US (+80%) stick out; main market Great Britain at -15%, Europe constant

- Wood consumption in construction expected to fall by 3 to 5% by end of 2020, and by another 3 to 5% in 2021

#3 AUSTRIA

- Possible slight decrease in softwood sawn timber production in 2020 (2019: 10.4 million m³); maybe reaching of last year’s production output

- Quality of log wood a challenge

- Big construction projects postponed this year, relaunch uncertain

- Sawn timber markets: very positive situation in DACH region, rest of Europe weaker; USA/China satisfactory/good

#4 FINLAND

- Softwood sawn timber production with a marked decrease to 10 million m³ in 2020, slight increase in 2021

- Sawmills’ performance better than predicted at the beginning of 2020 (thanks to DIY and renovation)

- Higher raw material costs than in Central Europe; volatile currencies and freights

- Byproducts and industrial wood are challenges due to a weak pulp market

* Reports of member countries (7/2020)