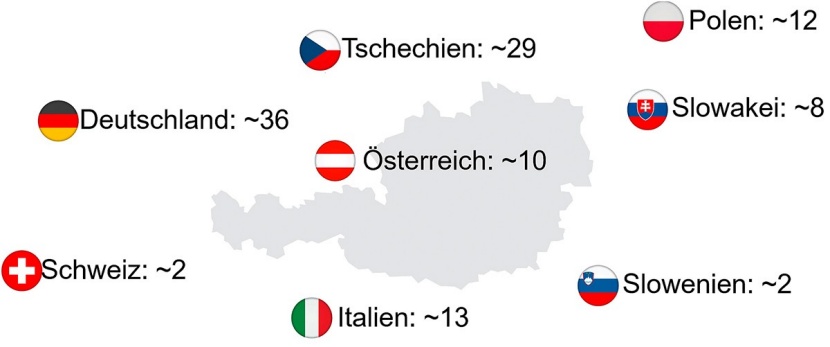

Damaged wood accrual 2018 in Austria and neighboring countries (in million sm³): In total, about 112 million sm³ accrued © Pöyry (data: Timber-Online/Fachverband Holzindustrie)

Accordingly, Austria's cutting volume of last year was increasing (19.2 million sm³; +8.4%). "The big "but" was that for the first time in history, more than 50% of the felling volume was damaged wood," Herbert Jöbstl, chairman of the Austrian sawmill industry, bewailed. Jöbstl referred to the challenge of distributing the local damaged wood volumes: "For lack of railway infrastructure, it is barely profitable to transport windfallen wood from East Tyrol to lower Carinthia. Germany manages to ship millions of solid cubic meters to China."

Once more, Jöbstl promised to sell as much as possible domestically despite transportation bottlenecks. "We additionally bought volumes worth the demand of three large sawmills within three years." Conversely, he called on his listeners' understanding for the fact that "also in the face of the crisis, long-standing partnerships with neighboring countries within the purchasing radius of sawmills have to be maintained."

"... not that dramatically poor"

Jöbstl seems to consider the fall of 2018 and the Q1 of 2019 the economic peak. The Global demand peak for softwood lumber has probably passed already. As for the prospects for the upcoming

months, Jöbstl pointed out that the construction business is usually affected later of decelerations. Here, forecasts are "not that dramatically poor". In Western and Eastern Europe, construction is expected to develop positively.

For Dr. Carl-Erik Torgersen, chairman of the Austrian timber trade, this is "complaining on a high level". Torgersen refers to global successes that "enabled us to boil down the dependency on the Italian market to only 43% of export volumes in 2018". Austria exported 5.9 million m³ at a production level of 10 million m³.

Torgersen referred to "volume discounts" in the sector with a surplus in goods: side boards. "This is how scarcity quickly turned into surplus", he judges the situation.

Back to global timber prices

The pricing charts for lumber and roundwood clearly show that roundwood prices dropped much more. "However, damaged wood is not only a cheap raw material. Currently, there are companies that receive 80 up to 90% of damaged wood – many sought-after products cannot be produced with that. We will have to place green wood into stock in order to have sufficient quantities next year." Furthermore, Jöbstl pointed out that for the first time since mid-2007, the Austrian roundwood price level is approximating the global market's level (= European Sawlog Price Index of the WRI). "This means that we do not have cost disadvantages compared to our Nordic competitors anymore," was Jöbstl's analysis.

260,000 sm³ per month for China

"New markets could now open up for Austrian producers," Torgensen concluded. China seems to be one feasible destination. With by now 120 million sm³/yr of softwood lumber imports, it is the world's biggest market. And Chinese buyers are flexible: Within only a few months, they built up an import flow of Central European damaged wood. "60,000 sm³ from Czech Republic and 200,000 sm³ from Germany are imported each month," Jöbstl presented the impressive numbers.

The times of raw materials abundance will at some point be over, especially for spruce. The Association of the Austrian Wood Industry wants to put the improvement of raw materials efficiency in the focus of future-oriented research. "We are the world leaders in product development. It is easy to copy. Austria must keep its headstart with new products."