US demand has not yet hit the peak

The US were the key market in 2020. Consultant Russ Taylor of Russ Taylor Global described the current market situation as “unprecedented”. Housing construction and the DIY sector grew last year. “From a demographic point of view, there needs to be more construction activity,” he analyzed. Nonetheless, with 82 million m³, demand for softwood lumber was still well below the peak consumption of 107 million m³ in 2005. The record prices recorded in 2020 are the result of 90% supplier Canada not being able to produce more.

Until 2023, US softwood lumber demand is going to rise further. A 4.5% increase is expected for this year alone. “These additional quantities are not going to come from Canada – which offers further opportunities for European suppliers,” predicts Taylor. In 2020, Canadian production decreased due to curtailments as a result of the coronavirus pandemic on the one hand and to sawmill closures in previous years and a scarcity in log wood on the other hand.

Binderholz in the Middle

In the US, additional production in sawmills is concentrated in the south and east of the country, i.e. exactly where Binderholz wants to start up the former Klausner production sites to reach an annual capacity of 1 million m³ each in the coming years.

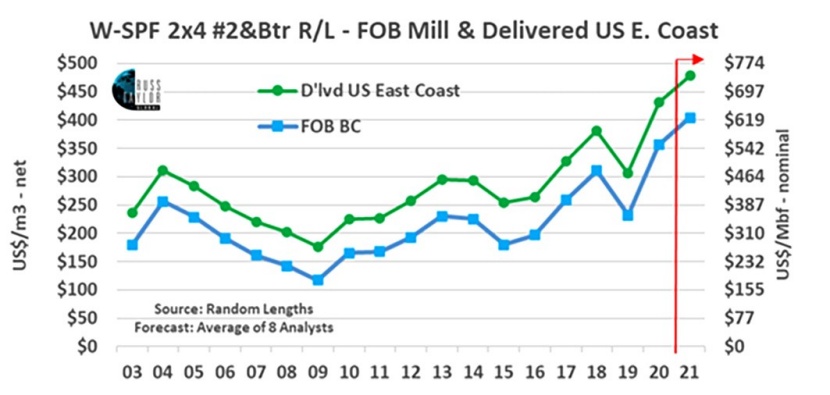

In 2020, Europe already satisfied 8.5% of the US’s softwood lumber import demand. The lumber arrives mainly on the high-priced East Coast, from where it is transported to the Midwest states. Taylor was flabbergasted at prices reaching $ 700/m³ for shipments to the East Coast in mid-February. Since November, the softwood lumber price has doubled, reaching a new record level. Even the lowest price recorded in November was far higher than what is usually considered normal. The situation is even more extreme with OSB: The price is three times the normal price and margins are even bigger than those of softwood lumber.

The result according to Taylor: In the third quarter of 2020, North American sawmills had EBITDA margins of 40%, and even 50% were reported by OSB producers.

Further price increases possible

US softwood lumber prices could rise again this year; green: in $/m³ © Russ Taylor Global

Price forecasts for 2021 vary greatly. On average, a further 12% increase compared to 2020 is imaginable (see chart). The futures predict $ 632/m³ ($ 979/1000 bft) at the end of March, and still $ 440/m³ ($ 682/1000 bft) in January 2022. “In the short term, there should not be a downward trend, which means that from 2020 to 2023, prices could reach the highest level ever recorded on the US market.”

Amir Rashad made a forecast for the Middle East and North Africa. In this region, he predicts a 4.5% increase in construction activity. After a weak year 2020 due to COVID-19, the fourth quarter of 2020 was characterized by a noticeable recovery which still lasts. Imports are expected to remain constant on all markets. However, consumption should rise on all markets – to a normal level.

Algeria is the MENA region’s second biggest market after Egypt. After a 5.2% decrease in 2020, GDP is expected to grow by 3.5% this year and by 2.4% in 2022. The devaluation of the Algerian dinar of 10% in three years, however, is going to make imports more difficult.

US market boosts prices in the Levant region as well

According to Rashad, there is demand for new softwood lumber shipments. Stock levels are currently very low – which is not expected to change unless shipments from Europe recover. Currently, the lumber crosses the Atlantic rather than the Mediterranean Sea. It is difficult to pay the world market prices, which would be necessary to fill up warehouses, though.

Sviatoslav Bychkov of Ilim Timber reported that Russian softwood lumber exports fell by 5% in 2020 to 29.4 million m³. Due to the scarcity of raw material, it was not possible to reach the record production of 2019 again. Furthermore, shipments to China decreased by 10%, reaching “only” 17.4 million m³. Main market China is increasingly going to receive goods via railway (One belt, one road). The growth in cargo is expected to reach 71% by 2025. The government is increasing its efforts to process more raw material in Russia, thereby bringing log exports close to zero. There will also be a number of sawmill and processing projects.

Production to increase in Central Europe

Christoph Kulterer, CEO of Hasslacher Norica Timber, presented the situation in Central Europe. Between 2015 and 2020, production grew by 12% in Germany, Austria and the Czech Republic. This year, output is to increase by around 1 million m³ (totaling 39.3 million m³).

Consumption remained stable at around 26.5 million m³ a year in the above-mentioned period, proving that the additional quantities of softwood lumber – an impressive 4.5 million m³ a year – were successfully exported.

Production grew mainly as a result of the massive accumulation of damaged wood, which Kulterer analyzed using Holzkurier figures. Now, in the first quarter of 2021, various factors have led to a certain scarcity of log wood especially in Austria. Nonetheless, Kulterer expects supply to be sufficient this year, albeit with higher log prices.

New productions a short-term problem

Since so many investments have been made especially in CLT and glulam productions, there could be a surplus in the short term. “In the medium term, however, the situation is going to be more balanced since demand for these products keeps rising,” Kulterer said optimistically.

Host Kai Merivuori was happy to see supply and demand increasing on world markets. “The challenge is that this is happening in various places. The global trade flows are changing at the moment”, he summed up.

Take care of the forests!

Merivuori ended his speech by calling on everyone to keep environmental aspects in mind. “We have to take care of the forests and keep them even more healthy and vital. Diversity should increase. This is 100% doable, if we seek cooperation with all stakeholders.”

Trends in 2021

#1 USA

- Demand for softwood lumber was at 82 million m³ in 2020 (record year 2005: 107 million m³).

- Expected increase in demand in 2021: +4.5 %

- Softwood lumber production in North America fell by 23 million m³ between 2005 (120 million m³) and 2019.

- European import share in the US in 2020: 8.5 %

- EBITDA margin in Q3 2020: sawmills 40%, OSB production around 50%

#2 Central Europe

- Softwood lumber production 2015 to 2020: +12% (AT, DE, CZ)

- 2021: +1 million m³ to 39.3 million m³

- Demand for softwood lumber 2015 to 2020: stable at around 27 million m³

- Currently scarcity in log wood (until Q2) and rising log prices

- Many investment projects in sawmills and processing plants

- Short-term surplus in glulam and CLT, in the medium term everything all right

#3 Levant region / Middle East

- Construction activity in the region could increase by 4.5 % this year.

- Algerian GDP in 2021 +3.5 % (2020: -5.2 %)

- Rise in world market prices reduces supply to this region

#4 Russia

- 5% decrease in softwood lumber exports to 29.4 million m³

- Exports to China: -10 % to only 17.4 million m³

- Log exports are to be reduced to nearly zero.

* Information gathered from speeches and contributions at the “Wood from Finland Conference 2021”